- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

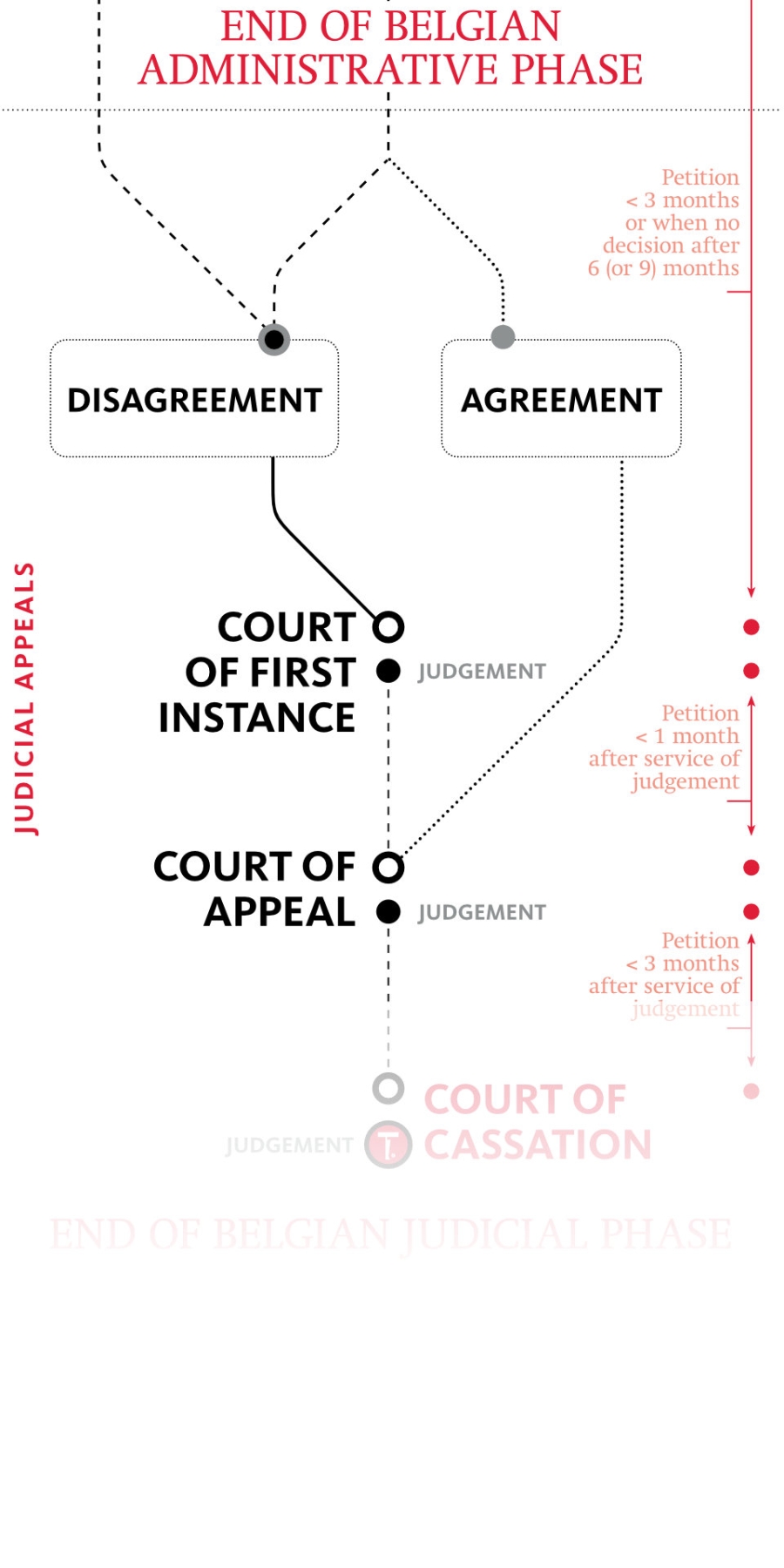

Any party dissatisfied with the judgement of the Court of First Instance, may appeal such judgement. The Court of Appeal has full jurisdiction to perform its own legal and factual analysis, and taxpayers may opt to be heard by 3 rather than 1 judge.

Both the taxpayer and the Belgian tax authorities – when dissatisfied with the judgement of the Court of First Instance – may decide to appeal against such judgement, and bring the case before the Court of Appeal (“Hof van Beroep” / “Cour d’Appel”), as long as the claim exceeds an amount of EUR 1,860.

It is critical to note that the appeal must be lodged within a timeframe of 1 month after the judgement of the Court of First Instance is served by the bailiff.

The general procedure before the Court of Appeal is the same as the procedure before the Court of First Instance:

It should be noted that the enforcement of the judgement of the Court of First Instance is suspended by the pending appeal, safeguard any uncontested portion of the judgement.

Furthermore, the Court of Appeal has full jurisdiction, meaning that if a legal matter is appealed, the Court of Appeal may replace the legal analysis of the Court of First Instance with its own legal analysis, and that if a factual issue is appealed, it can reverse earlier findings of the Court of First Instance.

Finally, it is worthwhile to consider, to opt for being heard by a chamber of 3 judges, rather than 1.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10