- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

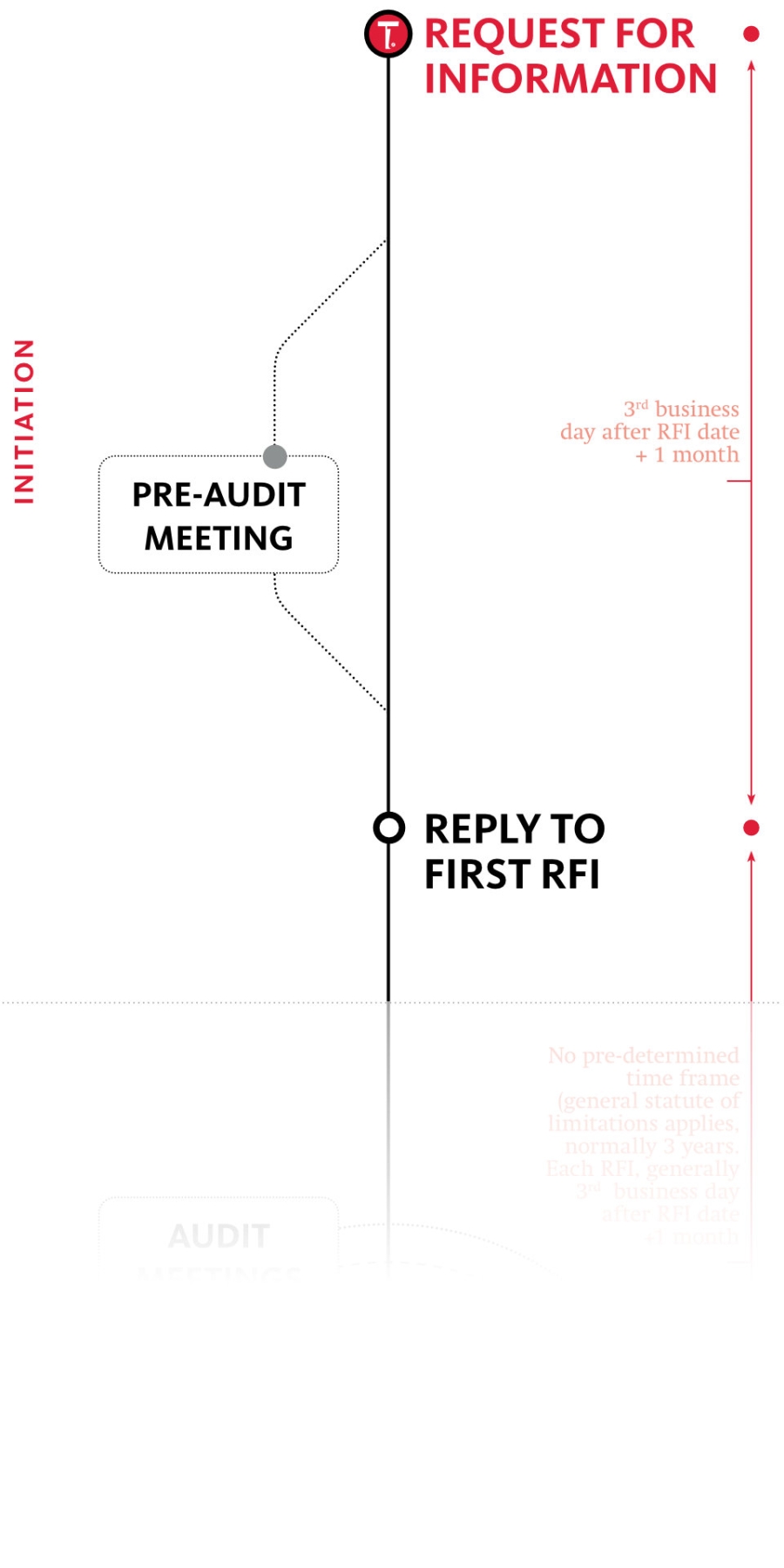

Keep calm and make a thorough assessment of the pertinence of the questions and the extent to which you have to address them in detail. The first, formal Request for Information (RFI) commonly initiates the TP audit process. This RFI typically consists of an extensive questionnaire, albeit increasingly tailored on the basis of submitted transfer pricing documentation and information obtained from other sources (most notably based on (global) exchange of information rules). However, in recent years, TP audits are more frequently initiated by means of tailor-made RFIs, and in some cases, even by an invitation for a pre-audit meeting (or a combination of both).

Upon being selected, a taxpayer typically will be warned of a transfer pricing audit being initiated through a formal, written RFI (“vraag om inlichtingen” / “demande de renseignements”) issued by the Belgian tax administration specialized transfer pricing cell. Alternatively, also other audit teams, such as the Large Companies team or the Special Investigation Squad may issue RFIs.

Today, we see two types of (rather extensive) transfer pricing questionnaires being issued to taxpayers:

In our view, when initiating the collection of the information, taxpayers should firstly keep calm when feeling overwhelmed by the general nature of certain questions and their potential reach. Furthermore, taxpayers should bear in mind the following attention points when deciding on the extent and detail provided to the Belgian tax authorities, and act in accordance with what the taxpayer specifically targeted can be knowledgeable of himself:

- Information stands for information, explanation or clarification. In this respect, the Belgian tax authorities are only entitled to ask for explanations on certain transactions. This logically presupposes that the tax authorities must have any knowledge of the transactions before it can ask for explanations. Fishing expeditions, however, are not allowed!

- In principle, questions can only relate to the normal investigation period of 3 years – i.e. the period when the tax return has been filed on time – but which can be extended to 10 years in case of tax fraud. Furthermore, as from tax assessment year 2023 new investigation and tax assessment periods have been introduced. Hence, questions can now also relate to the following new/extended investigation and tax assessment periods:

- A 4 year period in case of no filing or late filing of the tax return.

- A special period of 6 years in case of “semi-complex tax returns”, i.e. tax returns with a cross-border element (for taxpayers that have to file transfer pricing documentation (forms), in case of (reportable) cross-border transactions, in case payments are made to persons or establishments in non-cooperative jurisdictions, in case the tax return included an exemption/reduction of WHT based on a double tax treaty, the PSD or IRD, in case the tax return contains an imputation/credit of the lump-sum part of foreign taxes (FBB/QFIE), information received within the context of DAC 6/DAC 7,

- A special period of 10 years in case of “complex” tax returns (i.e. tax returns that relate to hybrid mismatches, the application of the CFC-rules, and cross border (tax planning) arrangements), and in case of suspected tax fraud based on a prior notification.

As of assessment year 2023, taxpayers are – in principle - also required to keep their records and bookkeeping for a period of 10 years (instead of 7 years).

- Questions must be targeted for investigating the taxpayer’s tax position

- Reference can only be made to transactions in which the taxpayer has participated

- No information can be requested on non-taxable income or expenditures and costs that have no legal effect

- The questions must be precise as they should not require infinite amount of research on the part of the taxpayer. This is to be assessed on a case-by-case basis. In general, questions should not interfere with the normal business operations of the taxpayer.

Without prejudice to the above, it is, however, important to not obstruct a tax investigation considering that the Procedural Law of 20 November 2022 has implemented the possibility for the tax authorities that the obstruction of a tax audit can be sanctioned by the competent court with a judicial penalty payment.It should be noted that these procedural principles are also applicable in case of a joint tax audit conducted in Belgium. Indeed, following the transposition of DAC 7 in Belgian law by the law of 22 December 2022, taxpayers have the same rights and obligations during a joint tax audit conducted in Belgium as in the case of a non-joint tax audit.

In the first RFI , ordinarily, an invitation is included to organize a so-called ‘pre-audit meeting’, which for taxpayers that have an issue with the general and open nature of the questions in combination with the attention points listed above may serve as a means for narrowing down the information to be provided, yet remaining in line with the obligation to cooperate with the Belgian tax authorities. It should be noted that the pre-audit meeting and the reply to the RFI are subject to certain formalities and timing constraints.

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10