- Help! I’m subject to a tp audit

- I want to prepare for a TP Audit

- Regulatory & Compliance

- Special Cases

- Insights

- Useful documents

Click to enlarge

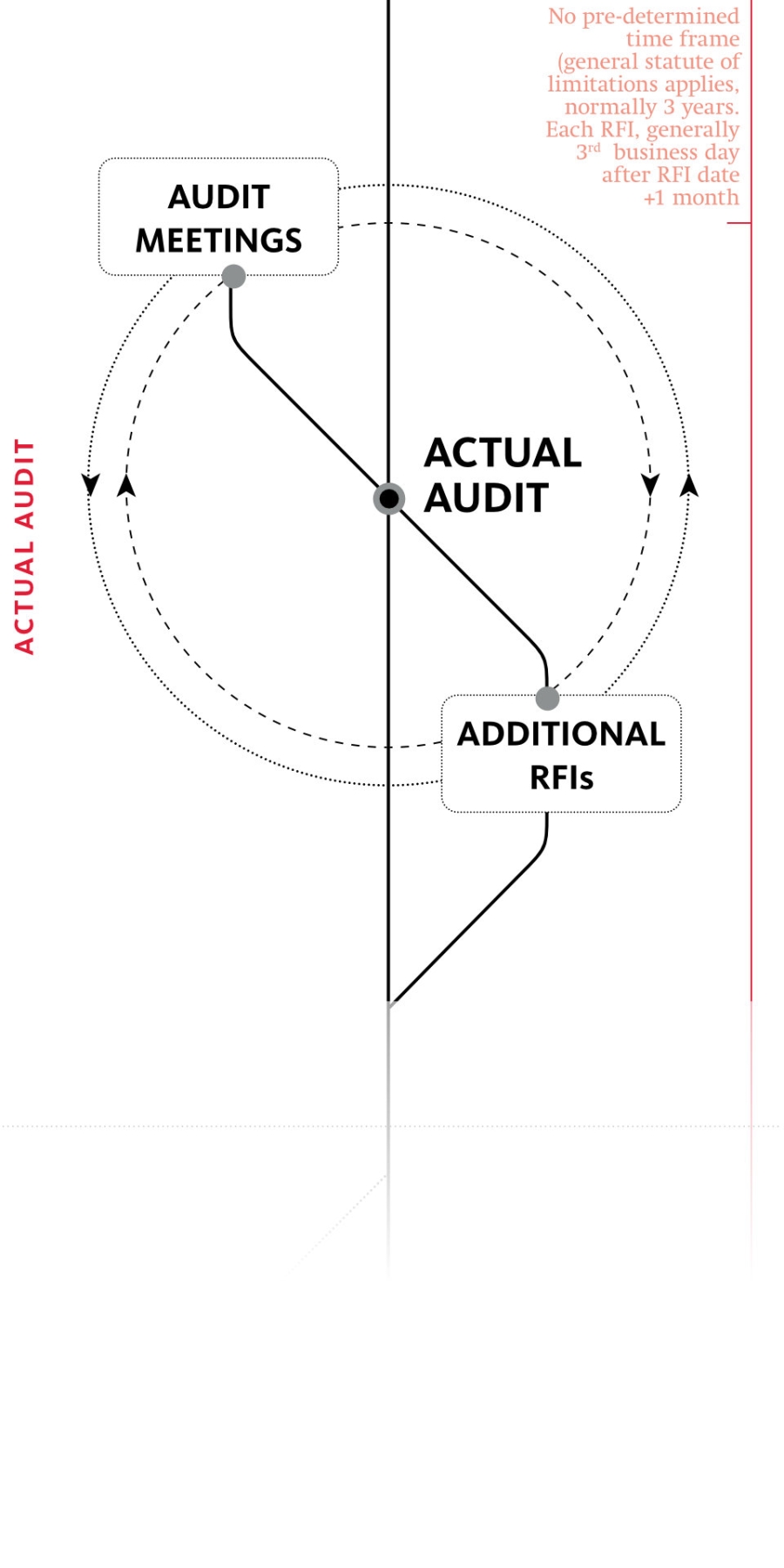

The actual audit typically consists of multiple rounds of meetings/on location visits and additional RFIs, and can drag on for months – a phenomenon we particularly observe in cases where there has not been a clear and open discussion with the tax authorities on the rule of law and the audit process in the beginning.

Typically, after having answered the first RFI, a second RFI is sent and the Belgian tax authorities make an appointment for a formal meeting. Indeed, in contrast to a pre-audit meeting this should be seen as an official visit to the taxpayers’ business premises.

Answering RFIs is not the only part of a taxpayer’s obligation to cooperate, but also accepting tax inspectors verifying the tax return at your business premises. Nevertheless, again, this is subject to certain formalities:

Now, in most instances, when it concerns a transfer pricing audit, such visits are planned for and accordingly do not come as a surprise. It is strongly recommended to ensure that the Belgian tax authorities are led to a separate meeting room immediately upon arrival, and do not leave that meeting room unattended. If it is being requested to do a tour, we strongly recommend to not honor such requests on short notice, but to prepare.

Nevertheless, the planned nature is not always the case, since the Belgian tax authorities have the right to visit your business premises unannounced – including for performing a transfer pricing audit. We refer to our separate section on a step plan in case of unannounced visits of the Belgian tax authorities, but can distill certain do’s & don’ts that in our view are also applicable during a regular, pre-announced visit:

DOs

- Accompany the tax inspectors to a meeting room to let them exercise their right to interrogate passively

- Answer questions that are overly broad (phishing expedition) with a question to be more concrete in return, and/or take time to think through answering

- Only convey information that is aligned with the topic(s) of the audit and tax year’s concerned

- Only give copies, and make a copy yourself of documents handed over

- Always ‘shadow’ the tax officials if they start walking around in the business premises

- Make note of any irregularities, and in case there are such irregularities, organise for an authenticated account (PV) drawn up

DON'Ts

- Hinder the investigation beyond the scope of your legitimate rights (mind the new possibility for the Belgian tax authorities to request the court to impose a judicial penalty payment in case of obstruction)

- Voluntarily give documents that were not requested (avoid own goals)

- Destroy or manipulate documents

- Leave documents lying around and exposed (clean desk during visit!)

- Sign documents without legal counsel

- Answer questions in a detailed manner and without careful consideration

- Allow interviews of other persons than the taxpayer

- Allow making copies themselves

- Allow opening cupboards, archives, etc.

- Allow review of documents without the presence of the taxpayer

Considering that multinationals generally have multiple types of intragroup relations and as transfer pricing is a complex topic and not an exact science, it should not come as a surprise that a transfer pricing audit actually consists of more than one RFI and audit meeting.

Moreover, there is no pre-determined period in which the tax authorities have to take a (final) position in the transfer pricing audit. It should be noted, however, that each time an RFI is issued the normal timeframe of 3 business days + 1 month applies (unless otherwise agreed upon). Typically, in our experience, the actual audit process takes about one year, but may be longer or shorter depending on the complexity of the audit. The only limit in this respect concerns the tax years that can be investigated in view of the Belgian statute of limitations which generally are:

Hence, generally, there is plenty of back-and-forth communication between the tax inspectors and the taxpayer, which at a certain point in time seems to be very frustrating for taxpayers since it appears that their does not come an end to the stream of information gathering. As mentioned earlier, however, being lenient in providing ‘excess’ information in the beginning of the audit process (for the sake of creating good vibes), in our experience has not been the right formula to have an efficient audit process in the end. Rather, our experience teaches us that an audit process that is governed from the beginning by a clear and pronounced model for cooperation based on the legal obligations and rights of both parties, tends to be more successful both in view of efficiency and efficacy.

If, nevertheless, the audit process seems to produce an unreasonable number of never-ending questions that seem to be going nowhere, for instance since you gave the inch in the beginning, and they are now are taking the mile, a few techniques could be of use, and have proven to be successful:

In the end, the tax authorities will have the final say in respect of their position to close the audit, and will issue a Rectification Notice (as starting point of the formal administrative procedure), unless there is full agreement that the tax return should not be reassessed. Also, when on the basis of the audit phase discussions described above lead to an agreeable outcome that nevertheless requires a reassessment of the tax return such Rectification Notice can be expected (to which then, in such case, one can simply agree in writing, upon which the Taxation Notice and Taxation follows).

Tour & Taxis

Havenlaan|Avenue du Port 86C B.419

BE-1000 Brussels

T +32 2 773 40 00

F +32 2 773 40 55

Grotesteenweg 214 B.4

BE-2600 Antwerp

T +32 3 443 20 00

F +32 3 443 20 20

23, Boulevard Joseph II

LU-1840 Luxembourg

T +352 27 47 51 11

F +352 27 47 51 10