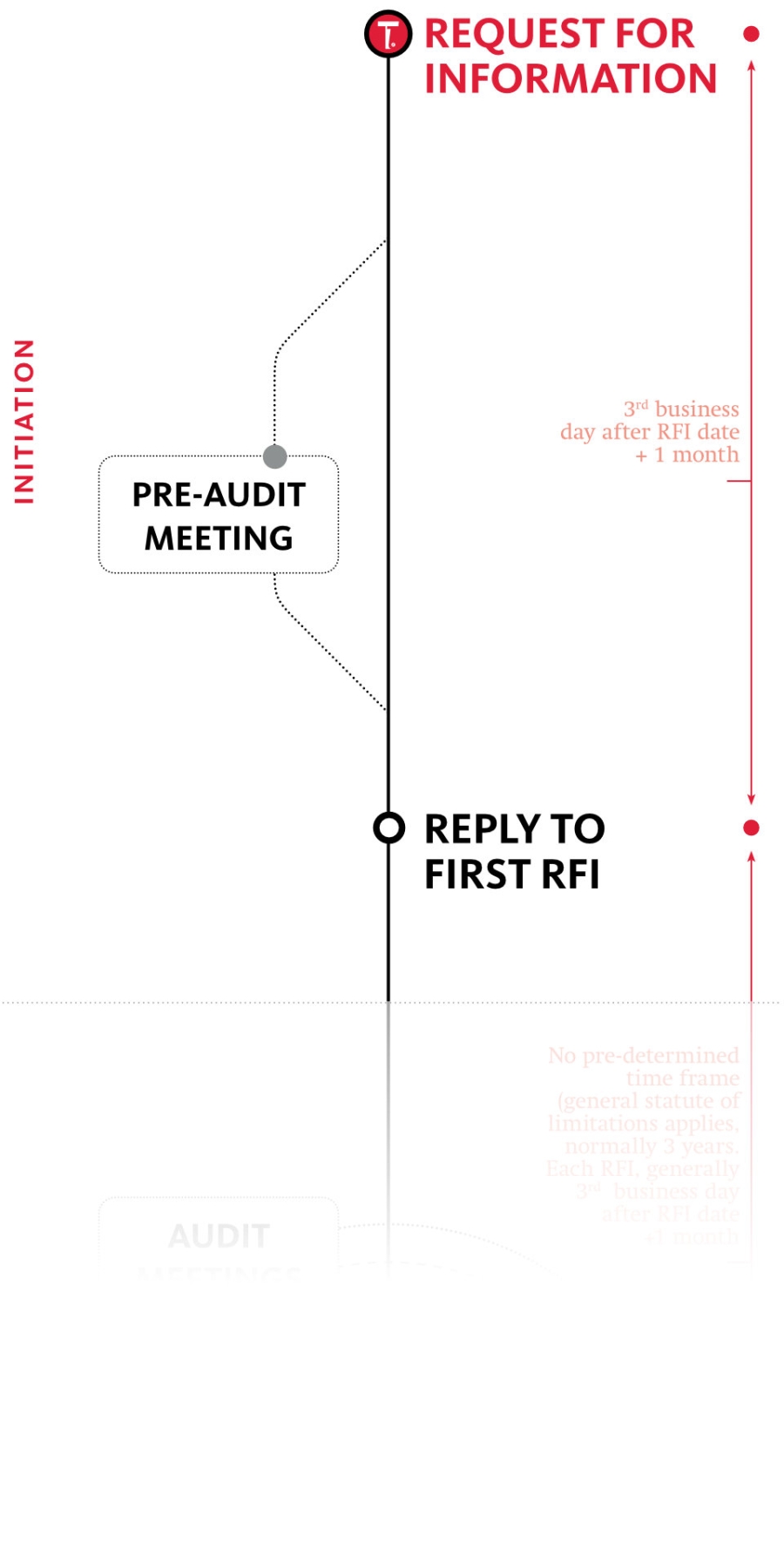

In the initial RFI, taxpayers may be invited to organize a pre-audit meeting to discuss the RFI, prior to responding to the RFI. There may be good reasons to do so, but also plenty of potential pitfalls.

A pre-audit meeting

Included in the first RFI, insofar that the TP audit was not already initiated by a pre-audit meeting, there may be an invitation to hold a so-called “pre-audit meeting” (and in pre-Covid-19 times optionally accompanied with an on-premises tour). A pre-audit meeting is a possibility for a taxpayer to discuss upfront, before the written reply to the RFI is due, the questionnaire received from the Belgian tax authorities. It is at the taxpayer’s discretion to request such a pre-audit meeting.

Accordingly, a logic question that follows, is: “Should I organize a pre-audit meeting?”

We have listed hereafter certain considerations to take into account.

- First of all, a pre-audit meeting should not be confused with an official visit to the taxpayers’ premises, which would allow for full access to business premises. When allowing for a pre-audit meeting visit, therefore, we do not generally recommend taking the Belgian tax authorities on a tour of the company, nor letting them talk to anyone outside the (prepared) team dedicated to the audit (such as employees, which is outside the competence of the tax authorities anyway as employees are not legally representing the company). Although a pre-audit meeting is not an official visit of the tax inspectors, any information that they pick up (with approval of the taxpayer) may still be valid for use against the taxpayer to build their case.

- Secondly, during the Covid-19 lock-down such physical pre-audit meetings were not organized on-site and physically, but through the means of web meetings. If – now and when physically pre-audit meetings are again possible – and a taxpayer could opt to organize such meeting, we recommend to (continue) organizing it in a non-physical manner as well if possible.

- Thirdly, one of the good reasons to request a pre-audit meeting may be that your transfer pricing policies may be covered by a ruling. Notwithstanding, the transfer pricing audit cell has the authority to audit whether the facts and circumstances underlying the ruling did not change, often this appears to be a good reason to downscale the scope of the audit. Being under such circumstance, we recommend not to await the pre-audit meeting, but to call to the inspectors to inform them about these circumstances and request them to alter the RFI in this respect or have them confirm in writing which questions they agree to be omitted.

- Fourthly, like having a ruling, it might be a good reason to request a pre-audit meeting if you have already been audited by another department of the Belgian tax authorities. Notwithstanding, the transfer pricing audit cell has the authority to reinitiate the audit process for topics that have already been audited by others before, often this appears also to be a good reason to downscale the scope of the audit. Again, being under such circumstance, we recommend not to await the pre-audit meeting, but to call to the inspectors to inform them about these circumstances and request them to alter the RFI in this respect or have them confirm in writing which questions they agree to be omitted.

- Most importantly, a pre-audit meeting (like any meeting) should have a clear and concise purpose. In respect of the previously mentioned attention points as regards the scope and nature of the information that can be lawfully collected by the tax authorities, in our view the taxpayer’s objective should be to agree upon with the tax authorities on an effective and efficient means of cooperation taking duly into account the rules of the game. Whereas arguably certain questions do not fully comply with those rules, we recommend showcasing disagreement with the RFI (and in particular in situations where the standard questionnaires have been sent, whilst the taxpayer has submitted transfer pricing documentation – a practice that according to our latest insights has diminished as they tend to be more tailor-made to a certain extent). We do not find it wrong that both parties around the table abide to the procedural rules, and are knowledgeable about that position, from the start. All too often we observe taxpayers acting very lenient in the beginning by responding to questions with information and details that are unlawful to request or to provide as the specifically targeted taxpayer, just to accommodate a friendly and cooperative environment of collaboration. All too many times this has led to a significant number of RFIs and meetings (cf. next phase, the actual audit) where the Belgian tax authorities keeps on coming back for more information, including non-public accounts, tax filings, corporate data of foreign affiliates, etc. You give an inch (2,54cm) and they’ll take a mile (1,609344 kilometers) unfortunately often applies, and the friendly climate also becomes a polar climate soon after frustrations boil up… Abiding to the rule of law nevertheless is something that company directors should be conscious of in view of directors’ liability. At least, making the point clear that as a taxpayer one intents to be fully cooperative with due respect for the rule of (not only tax) law should be (one of) the key objective(s) of the pre-audit meeting. However, in our view, this could also be incorporated in the reply to the RFI.

- A final objective of the pre-audit meeting may be to discuss the down scoping of the questions. Indeed, inspired by Circular Letter nr. Ci.RH.421/580.456 (AOIF 40/2006) dd. 14.11.2006, a pre-audit meeting should be means to discuss and retain the relevant topics (only). Whereas it is true that during pre-audit meetings questions that are fully irrelevant tend to get excluded, it is also our experience that eventually more additional information is being requested during the pre-audit meeting than stated in the first RFI initiating the audit. Going back to the previous topic, again, one could ask whether such practice is in line with the general principle of good government that dictates demands for information should be moderate and carefully considered.

Conclusion? There is not one conclusive answer for everyone, but we can stress not deciding lightly on whether or not requesting the invitation of organizing a pre-audit meeting. It should be carefully assessed whether or not do so: anticipated benefits vs. incremental risks of initiating a snowball effect on information to be produced, or even giving company-own insights that lawfully would not be required to being disseminated to the Belgian tax authorities, with the potential adverse consequence of not only undermining your own tax filing position, but also jeopardizing breach of company secrecy and/or breach of director’s liability.

Our recommendations in a nutshell

In any case, if one wishes to pursue organizing a pre-audit meeting, we strongly recommend keeping it virtual, having a clear agenda including a clear statement on the method of collaboration, in any case only conveying information that is publicly available (like a very general presentation) and not trying to answer the questions raised in the RFI already except for those that are totally irrelevant - your focus should be on downscaling the information to be provided whilst not accepting new requests for information to be answered within the same applicable time frame (best practice would be to request for a new written RFI, with a new applicable timing). In order for you to assess the need to have a pre-audit meeting, we have listed hereafter the pros and cons of organizing it:

PROs

- Being in control of setting the scene for how the collaboration should work

- May improve understanding of the tax authorities when reading the formal written replies later subsequently

- Potential limitation of questions that are considered as irrelevant or already sufficiently responded to, and hence no further detailed formal reply is needed (yet to be repeated in formal reply)

CONs

- Could smell like a (disallowed) phishing expedition?

- In case of a physical meeting, uncontrolled access to information may be granted, or wrong impressions might be given

- Most of the times a written reply on the full questionnaire is expected anyway

- Risk adding additional questions to the initial questionnaire, without due care of rules of law (beyond scope)

- As such pre-audit meeting does not buy time for drafting a reply to the RFI